Undergraduate Student Loans

Loans to support college expenses.

Loans to support college expenses.

The Undergraduate Student Loan Program provides interest-free loans of up to $7,500 to low- and moderate-income residents of New York City’s five boroughs, Westchester, or Long Island to help pay undergraduate education expenses.

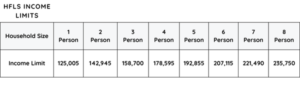

Loan applicants must have annual pre-tax household income at or below the income limits for their household size. If your annual pre-tax household income is slightly above the limit in the chart below, please contact Loan@HFLS.org to speak with a Loan Officer about your specific situation; you may still qualify for an HFLS loan.

The student’s parents are typically the borrower, unless the student is financially independent. A borrower may take one Undergraduate Loan per academic year over up to four years that the student is in school. Students must have completed a Free Application for Federal Student Aid (FAFSA) prior to submitting an HFLS loan application.

Loans are repaid in 25 installments of $300/month; one loan is repaid at a time in the order in which they are taken. If an independent student is the borrower, the monthly repayment amount is based on ability to repay until three months after the expected graduation date, at which time the monthly repayment will be $300/month until the loan is fully repaid.

All loans have a one-month grace period before repayments begin. Repayments are made on either the 5th or the 20th of each month; borrowers select their preference before HFLS disburses the loan. All loan repayments are made by electronic debit of a checking account.

Since HFLS lends to households, a married couple is considered one borrower. If an applicant is married or partnered, he or she must include their spouse’s/partner’s information in the application.

One guarantor is required for the first Undergraduate loan of up to $7,500. For each additional loan, two guarantors are required, and both guarantors must complete Guarantor Forms. Borrowers may use the same guarantors on additional Undergraduate Loan applications given that they still meet all eligibility requirements.

A married couple is considered one guarantor. If a guarantor is married or partnered, his or her spouse/partner must also complete and sign the Guarantor Form.

Each guarantor is “jointly” and “severally” liable for the loan in the event a borrower is unable to pay for any reason. This means that, while HFLS would expect each guarantor to share equally in the responsibility of repaying the loan, each is legally liable for the full amount, and any one guarantor could be called upon to repay the balance due.

Guarantors must meet the following criteria:

Even if they meet the requirements above, the following people may not guarantee a loan:

From the borrower:

From the guarantors:

After receiving the completed application, required documents, guarantor form(s), and ID-Pal verifications, an HFLS Loan Officer will contact you to request any missing information and schedule a 15-minute loan interview by phone.

During the interview, the Loan Officer will ask any questions they have about your application, explain the loan closing process and loan terms, and answer any questions you have.

Due to the high volume of applications, we ask that you do NOT contact HFLS about the status of your application. HFLS reviews complete applications only in the order in which they are received. If you have not heard from a Loan Officer, it is because one or more of the steps above is not complete or because HFLS is processing applications that were completed before yours.

The information and documents below are required for an Undergraduate Student Loan.

From the borrower:

From the guarantors:

After receiving your online loan application and guarantor forms, an HFLS Loan Officer will contact you to schedule a 15-minute loan interview (by phone).

During the loan interview, an HFLS Loan Officer will review your application and other required documents with you, determine whether any additional information is needed, explain the loan closing process, and answer any questions you have.

Due to the high volume of loan applications received by HFLS, we ask that you please do not contact HFLS

HFLS reviews and decides on loan applications daily. If we have questions about your application or guarantor, you may receive a call or email from a Loan Officer asking for further information before HFLS will make its decision.

HFLS, in its discretion, may decline to make a loan, make a loan in an amount less than that requested, or require different or additional guarantors.

If your loan is approved, you will receive an email with loan closing documents for you to complete and sign electronically via DocuSign. The loan closing paperwork includes:

Once HFLS receives the electronically signed documents above, we will disburse your loan funds directly into your checking account within three business days. (Please note that it may take a few extra days after the disbursement for the loan funds to appear in your checking account.)

![]()

![]()

![]()